Market Snapshot

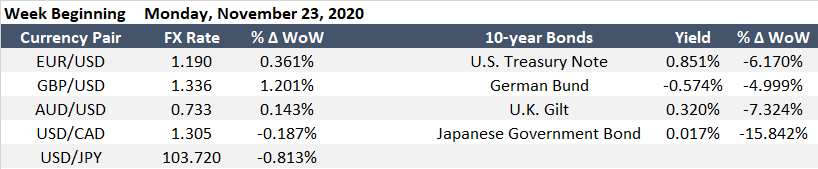

Market participants are preparing for a shortened trading week due to the Thanksgiving Holiday on Thursday and an early close on Friday. Market sentiment opening RISK-ON as another Monday of positive vaccine announcements are made with the latest coming from AstraZeneca. S&P 500 futures are pointing to 0.40% higher at the open to 3,569 and the 10-year U.S. Treasury yield is up 2.1bps to 0.85%. WTI Crude is up over 1% to $42.88/barrel.

The shortened trading week will see a total of nearly $200 billion of two-year, five-year, and seven-year U.S. Treasury auctions, including floating-rate notes, crammed into Monday and Tuesday. November FOMC Minutes is scheduled to be released on Wednesday.

Fed to “Return” Funds to Treasury

Last week, U.S. Treasury Secretary Steven Mnuchin asked Federal Reserve Chairman Jerome Powell to “return” billions in relief funds that it hadn’t deployed as part of its Main Street Lending Program (MSLP). Market participants largely shrugged off the headline as MSLP remained largely untapped by small business owners, likely because terms of the alternative PPP funding were comparatively more attractive with a portion being forgiven. While the Fed has agreed to “return” the billions in untapped funds, to be clear, there is no barrel of cash to return. Mnuchin, ostensibly, may make another push for fiscal stimulus before year-end as the headline of billions being released back to the Treasury may move to sway some Senators to backing a larger stimulus package.

Treasuries Remain Resilient

As U.S. election volatility has largely dissipated, investors attempt to balance the short-term novel coronavirus headwind with a long-term tailwind economic outlook in a post-covid environment with numerous vaccines.

While equity investors are rotating into cyclical industries, higher U.S. Treasury yields and loosening of credit markets are being tempered by near-term expectations that the Fed will continue to be supportive and may announce a shift in its asset purchases as soon as next month during the December 15-16 meeting. Expectations that the Fed’s $80billion of monthly asset purchases may shift to the long-end of the curve, will cap the rise of long-term yields. Watch for success in additional fiscal stimulus and vaccine efficacy and deployment/uptake as both measures will be inflationary.

Over the weekend, Saudi Arabia hosted the Group of 20 (G-20) Summit where global leaders pledged to “spare no effort” in ensuring affordable global access to COVID-19 vaccines and to halt debt repayments from poor countries. Looking ahead to 2021, expect conversations and potential agreements on a multilateral trading system, international taxation on multinationals, and continuing to address climate change and biodiversity loss.

Weighing heavily on the broader market are:

- U.S. fiscal stimulus package

- A fiscal stimulus package is unlikely to occur until Q1 2021, though U.S. Treasury Secretary Mnuchin may make another push before year-end.

- We may see long-end rates push significantly higher, on inflation expectations, should Congress agree on a $2 trillion+ fiscal stimulus plan.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- The Trump administration banned investments in companies controlled or owned by China’s military. Current investors will have until November 11, 2021, to comply with the ruling that goes into effect on January 11, 2021.

- Second/Third novel Coronavirus wave

- With COVID-19 cases surging, Europe is grappling with various stages of lockdowns while the U.S. is implementing restrictions with some localities eyeing lockdowns again.

- While there are numerous COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.

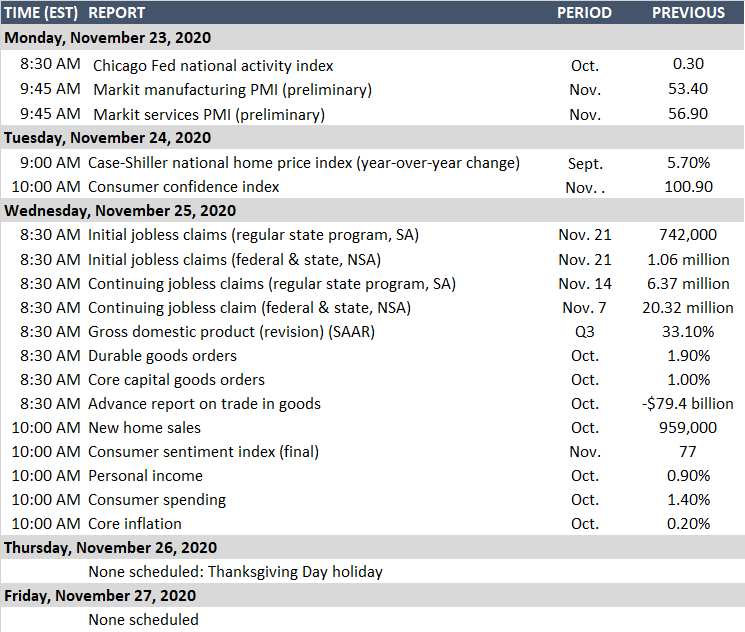

Upcoming Economic Data This Week: