Market Snapshot

U.S. Treasury yields are opening nearly 1bp higher on the final trading day of November while equity futures point to a lower open after the Trump administration announced plans to add China’s SMIC, a semiconductor manufacturer, and energy company CNOOC to a trading blacklist. Investors may seek to close out the month by taking some gains off the table before rebalancing their portfolio in December for a “Santa rally”.

WTI Crude oil is down nearly 2% to $44.73/barrel this morning a preliminary OPEC+ meeting did not result in a compromise between Saudi Arabia and Russia. and could fall further should OPEC+ fail to agree later today to continue its 7.7mm cut to daily output for 2021.

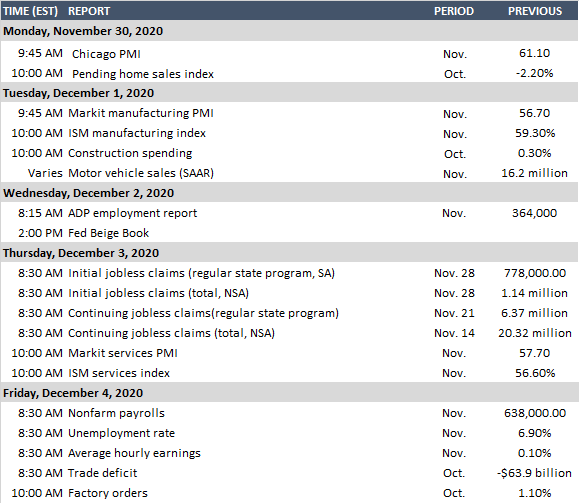

The two events to watch for this week will be Federal Reserve Chairman Jerome Powell’s testimony before Congress on Tuesday and Wednesday and the U.S. employment report on Friday.

Janet Yellen Is Back

Though U.S. equity markets and the U.S. Dollar Index jumped last Monday following news of President-Elect Joe Biden’s apparent selection of Janet Yellen as Treasury Secretary, U.S. Treasuries remain relatively unmoved by the announcement. Bond investors may recall that Ms. Yellen’s time as Federal Reserve Chair was filled with dovish monetary policy. Investors are currently more concerned about the continued impact on the broader economy from the novel coronavirus and the timing of the vaccine rollout.

On fiscal policies, not unlike current Treasury Secretary Steven Mnuchin, Ms. Yellen has said recently that the economic recovery will be uneven and lackluster if Congress doesn’t provide additional fiscal stimulus to combat unemployment and keep small businesses afloat. While the current economic situation may warrant additional stimulus, just last year, Ms. Yellen said that the federal budget deficits were on an unsustainable path. Her “magic wand” solution at the time was to raise taxes and cut retirement spending. Other issues that Ms. Yellen has spoken often over the past year include:

- Supporting carbon taxes, in an effort to reduce greenhouse gas emissions and tackle climate change.

- Improving bank supervision. We expect her to address risks that threaten the broader financial system such as increased indebtedness by nonfinancial corporations (eg: private equity and hedge funds).

- Addressing China’s subsidies for state-owned enterprises and competition on new technologies with significant national security implications.

It is widely expected that Ms. Yellen would breeze through Senate confirmations as both sides of the aisle appreciate her matter-of-fact approach to economic policies. With current Fed Chairman Powell and Yellen aligned, some investors believe the Fed will adopt a form of yield curve control where long-end rates are kept artificially low as former Fed Chairman Bernanke similarly executed operation-twist in 2011. However, investors should keep in mind that operation-twist was designed to stimulate the housing market after the housing bubble burst in 2008.

Weighing heavily on the broader market are:

- U.S. fiscal stimulus package

- A fiscal stimulus package is unlikely to occur until Q1 2021, though U.S. Treasury Secretary Mnuchin may make another push before year-end.

- We may see long-end rates push significantly higher, on inflation expectations, should Congress agree on a $2 trillion+ fiscal stimulus plan.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- The Trump administration banned investments in companies controlled or owned by China’s military. Current investors will have until November 11, 2021, to comply with the ruling that goes into effect on January 11, 2021.

- China’s top chipmaker SMIC and national offshore oil and gas producer CNOOC likely to be added to the blacklist.

- Second/Third novel Coronavirus wave

- With COVID-19 cases surging, Europe is grappling with various stages of lockdowns while the U.S. is implementing restrictions with some localities eyeing lockdowns again.

- While there are numerous COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.