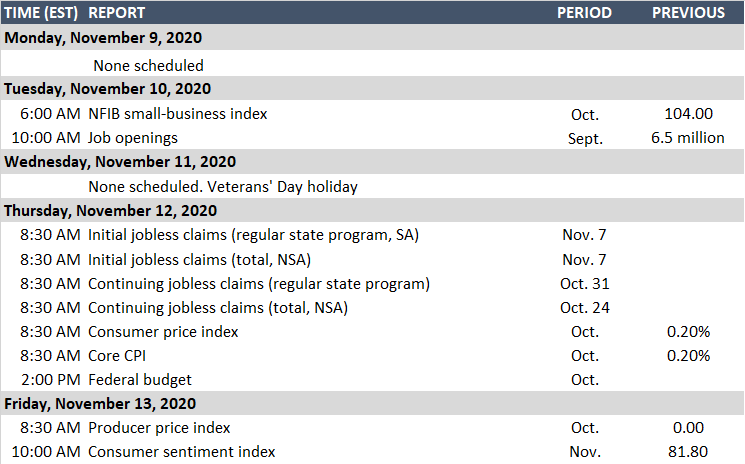

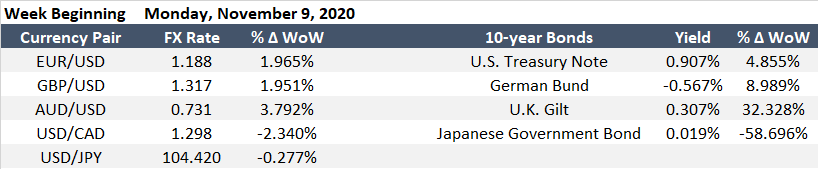

Market Snapshot

Volatility continues this morning as the 10-year U.S. Treasury yield continues to flip between gains overnight during Asia trading hours to opening lower during Europe trading hours – though stabilizing and moving 10bps higher near the New York open after Pfizer just made headlines that its COVID-19 vaccine is 90% effective. The USD is trading lower against its G8 peers and WTI crude oil is finding a floor and trading higher this morning at $38/barrel. Equity futures continue to be risk-on with investors seemingly elated over the election results of a divided government and expectation of lower rates for longer with little to no impact on corporate taxes.

Job Market Recovery Continues to Impress

Last Friday’s non-farm payrolls showed an impressive print of 638,000 jobs created in the month of October, despite a 147,000 drop in temporary census employment.

- Private payrolls saw gains of 906,000, up from 892,000 in September

- 271,000 jobs were created in the hospitality sector and remain much stronger than the traditional heavy end of the summer travel season (August).

- The unemployment rate fell all the way down to 6.9% from 7.9%. Comparatively, it took nearly five years after the global financial crisis of 2008 to recover to the same levels.

Fed Stands Pat

Last Thursday, Chairman Powell and committee members made the predictable decision to stand pat and keep rates and policy unchanged. The post-meeting policy statement noted that “economic activity and employment have continued to recover” and that “the path of the economy will depend significantly on the course of the virus”. Of concern will be whether the recent surge in COVID-19 infections in the Midwest result in a drag on the domestic economy, as the states have yet to implement the sort of draconian lockdowns currently being imposed across Europe.

Fed Chairman Powell described fiscal support as “critical” and “absolutely essential” during his press conference. Without additional fiscal support, the pressure will be back on the Fed to find ways to support the economic recovery likely via an expansion of its large-scale asset purchases on longer-term debt.

USD Rates Extremely Volatile

The probability of a “blue wave” election outcome has since diminished with the weekend press announcement of Joe Biden as the 46th President-elect and instead looks likely to be a divided government. It is still possible for a fiscal stimulus deal to be reached during the lame-duck session, although the overall size is likely to be between $1.5 trillion and $2 trillion, rather than the $2.2+ trillion that would have been anticipated if the Democrats had also flipped control of the Senate.

Interest rate volatility was high and saw long-term rates whipsaw between daily gains and losses during the runup to election day. Following election-day, long term rates pared back its gains, with the 10-year U.S. Treasury rate falling 20bps from 0.93% pre-election to 0.73% on Thursday before recovering 10bps on Friday.

Weighing heavily on the broader market are:

- U.S. fiscal stimulus package

- A fiscal stimulus package is unlikely to occur until Q1 2021.

- We may see long-end rates push significantly higher, on inflation expectations, should Congress agree on a $2 trillion+ fiscal stimulus plan.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- Second novel Coronavirus wave

- The Midwest is experiencing a large second wave of the virus though has not implemented lockdowns, unlike Europe.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.