U.S. equities are trading higher this morning with the S&P500 index up 12.12 points to around 3,385 +0.36% following gains that began in Asia and are continuing during European market trading. The 10-year U.S. Treasury rate is -2.3bps lower to 0.687% after gaining over the past few weeks. WTI crude oil is +0.26% to 42.115 per barrel. Gold spot prices are at 1,983.50, about 1.73% higher.

China’s Central Bank

China’s central bank, The People’s Bank of China or PBOC, provided liquidity to commercial lenders earlier this morning to help them manage upcoming government bond issuances as the economy recovers.

- The PBOC added 700 billion yuan or nearly US$101 billion of one-year funding via its medium-term lending facility. The central bank said last Friday that today’s operation is meant to offset the 400 billion yuan in loans coming due today and another 150 billion yuan maturing on August 26.

- The central bank last week offered the most short-term funds since May, replenishing a banking system that needs about $500 billion this month.

- USD/CNY fixing down 0.06% at 6.9362.

U.S. Treasury Yields Reach 5-Week High

While rates are slightly lower by about 2bps this morning, the 10-year and 30-year U.S. Treasury yields continued is climb higher last week to 0.71% and 1.45%, respectively. The 10-year is 15bps higher and 30-year is 22bps higher since the beginning of August while short-term rates remain relatively unchanged. The 2-year note rose 3bps to 0.14% since the start of the month.

Driving yields higher was an influx of new debt issuances last week, with broker-dealers bidding yields higher to ensure a successful auction.

- The U.S. Treasury Department sold a record $38 billion of 10-year Notes with strong demand.

- July CPI inflation rose +0.6% versus expectations of a +0.4% increase.

- Last week’s jobless claims dipped below one million for the first time since March.

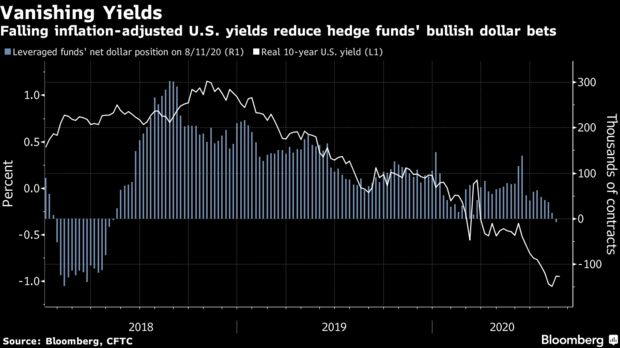

USD Weakness

The world’s reserve currency of choice, the U.S. Dollar (USD), continued to fall against its biggest peers with the Euro rising against the USD the most in a decade. With U.S. assets looking less attractive on a risk-adjusted basis after the Fed’s near-zero rate policy and “unlimited” asset purchases, hedge funds net positions show a growing bullish bet on the Euro currency. The increasingly crowded trade is a sign that investor confidence is waning in the U.S. ability to weather the coronavirus pandemic outbreak and that other major economies are better able to cope.

Weighing heavily on the broader market are:

- A comprehensive stimulus package before September remains elusive, leaving the U.S. economy on the fringe.

- The U.S.-China relations show little sign of easing, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus. The virtual meeting was initially scheduled to be held this past Saturday but has since been delayed with no future date set.

- Uncertainty and the prospect of a drawn-out and heavily litigated November presidential election.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.

Up ahead this week:

Wednesday:

- The Energy Information Administration (EIA) will report the latest crude oil inventory.

- A review of the OPEC+ agreement will be held by the Joint Ministerial Monitoring Committee.

Thursday:

- Be on the lookout for weekly U.S. jobless claim for the period ending August 15 (last Friday).

- The PBOC will announce China’s latest loan prime rate (one-year currently at 3.85%).

- A cut may spook markets as it would be a sign of a further slowing economy.

- A review of the OPEC+ agreement will be held by the Joint Ministerial Monitoring Committee.

Friday:

- We will receive data on PMIs in the Euro-area and Japan.