Historically, the month of August tends to hold steady as traders and investors alike take time off before post-Labor Day trading begins. However, given the fluid coronavirus situation and its impact on the global economy coupled with increasingly tense geopolitics, we expect continued volatility throughout the month across most asset classes.

Investors continue to flock to safe-haven assets amid the uncertainty about the economic recovery and the timing for a safe and effective COVID-19 therapeutic or vaccine. Still, equities have gained four straight months in a row with the S&P 500 gaining 5.1% in July, the Dow and the Nasdaq Composite have gained 2.38% and 6.82%, respectively. In the fixed income rates market, the investor sentiment was, comparatively, more subdued with the 10-year U.S. Treasury closing the week 6bps lower to 0.54%. Gold Futures spiked to an all-time high of $2,005.4/ounce last Friday, crossing the $2,000 level for the first time.

Weighing heavily on the broader market were:

- Unemployment benefits expired Friday with Congress and the White House seemingly far apart on an agreement.

- Exxon Mobil, Chevron, and Royal Dutch Shell reported worse than expected losses as lower oil prices coupled with significantly reduced demand.

- Consumer sentiment deteriorated this month amid a resurgence in new coronavirus cases, The University of Michigan’s consumer sentiment index came in at 72.5 for July, down from June’s 78.1.

- The U.S. Gross Domestic Product (GDP) collapsed by -32.9%, the deepest decline ever recorded (since 1947).

The world’s reserve currency of choice, the U.S. Dollar (USD), continued to fall against its biggest peers with the Euro rising against the USD the most in a decade. The British pound headed for its best July since 1990. Currency traders, already concerned over falling U.S. Treasury rates, real yields near all-time lows, and disappointment over the U.S. response to the coronavirus, shifted away from the greenback after U.S. President Trump raised the idea of delaying elections this year resulting in every major currency in the world rising against the U.S. Dollar.

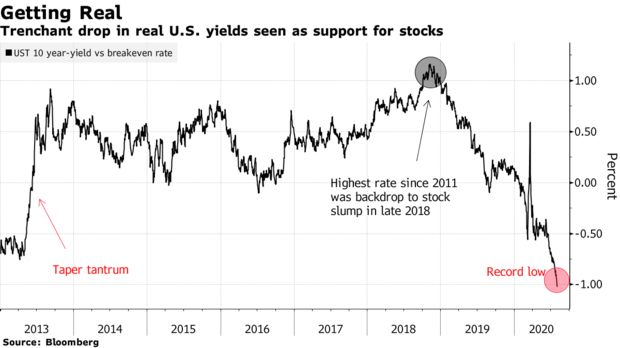

Real Rates and the Fed

Real rates, inflation-adjusted yields, have sunk to a record low, near -1%. As the Fed is “not even thinking about thinking about raising rates.” The Fed’s pledge to keep rates low has been a tailwind for equities and precious metals. Conversely, the lower yields have depressed lending margins.

- The FOMC concluded its two-day meeting last Wednesday and voted unanimously to hold interest rates steady, maintaining the Fed Funds target range between 0% and 0.25%, as expected.

- Committed to maintaining its bond purchases and lending programs, as needed.

- Will continue to extend dollar liquidity swaps and temporary repo operations through March 31, 2021.

- The closing statement summarized the current economic growth as better than it was back in March but still subpar:

- “Following sharp declines, economic activity and employment have picked up somewhat in recent months but remain well below their levels at the beginning of the year,” the statement said. “Weaker demand and significantly lower oil prices are holding down consumer price inflation. Overall financial conditions have improved in recent months, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.”

- We look forward to the Fed’s upcoming September meeting for updated guidance about the path of interest rates based on its strategic review on inflation.

Up ahead this week:

- Tuesday: The Reserve Bank of Australia makes its interest rate decision.

- Thursday: The Bank of England and Reserve Bank of India makes its interest rate decision.

- Friday: U.S. Jobs data for July is expected to be released.

Fed Speak:

- Monday: St. Louis Fed President James Bullard, Chicago Fed President Charles Evans, and Richmond Fed President Tom Barkin.

- Thursday: Dallas Fed President Robert Kaplan.