Market Snapshot

U.S. equity futures point to a higher open following Asian and European equities after a report that White House officials have reassured American businesses that a ban on the WeChat won’t be as broad as feared. WeChat’s parent Tencent Holdings Ltd. rallied 5.8% to HKD 548 at the close in Hong Kong. Further fueling investor sentiment is news that the Trump administration may fast-track vaccines and treatments for the novel coronavirus. S&P 500 futures are up +0.86% pointing to an open of 3,421.75. WTI crude oil is trading +0.76% higher to $42.66 as hurricane Marco and Laura are rolling toward the U.S. Gulf Coast shutting nearly 58% of crude production. U.S. Treasuries are nearly unchanged from last Friday’s close with the 10-year Note +0.004% higher to 0.641% as traders hold steady for Fed guidance.

Jackson Hole Symposium

The world’s most heavily traded bond market enters a potentially pivotal week with interest rates, inflation, and the economy at the forefront as investors look for signals from the Fed on its next crucial policy move. Federal Reserve Chairman, Jerome Powell, is expected to kick-off the annual economic forum beginning Thursday. Traders will be listening closely to the Fed’s long-awaited monetary policy framework review focusing on a new inflation strategy and any updates to its bond-buying program.

Since 1978, the Federal Reserve Bank of Kansas City has sponsored a symposium on an important economic issue facing the U.S. and world economies. This year, the topic will be “Navigating the Decade Ahead: Implications for Monetary Policy.”

The Fed’s annual economic forum will be live-streamed on Thursday and Friday (August 27-28). For more information on the event and history, please visit: https://www.kansascityfed.org/publications/research/escp

USD Rebounds

The world’s reserve currency of choice, the U.S. Dollar (USD), rebounded after last Wednesday’s release of the July 28-29 FOMC meeting minutes. The minutes revealed that the Fed is concerned about “the ongoing public health crisis which would weigh heavily on economic activity, employment, and inflation in the near term.” The committee added that providing forward guidance “would be appropriate at some point,” and dismissed yield-curve control, saying that “yield caps and targets would likely provide only modest benefits in the current environment.”

With the crowded short USD trade, investors took the opportunity to take profits as the mildly dovish minutes were not as aggressive as some had hoped would be. The rebound continued into Friday as EU data missed expectations while in the U.S. robust home sales and improving activity at manufacturers and service providers indicate a firmer path for a U.S. economic recovery.

- EU Manufacturing PMI contracted to 51.6 from 54.9 in July, a two-month low.

- EU services output was down to 50.1 from 54.7.

- The flash IHS Markit Eurozone Composite PMI posted 51.6, down from July’s reading of 54.9.

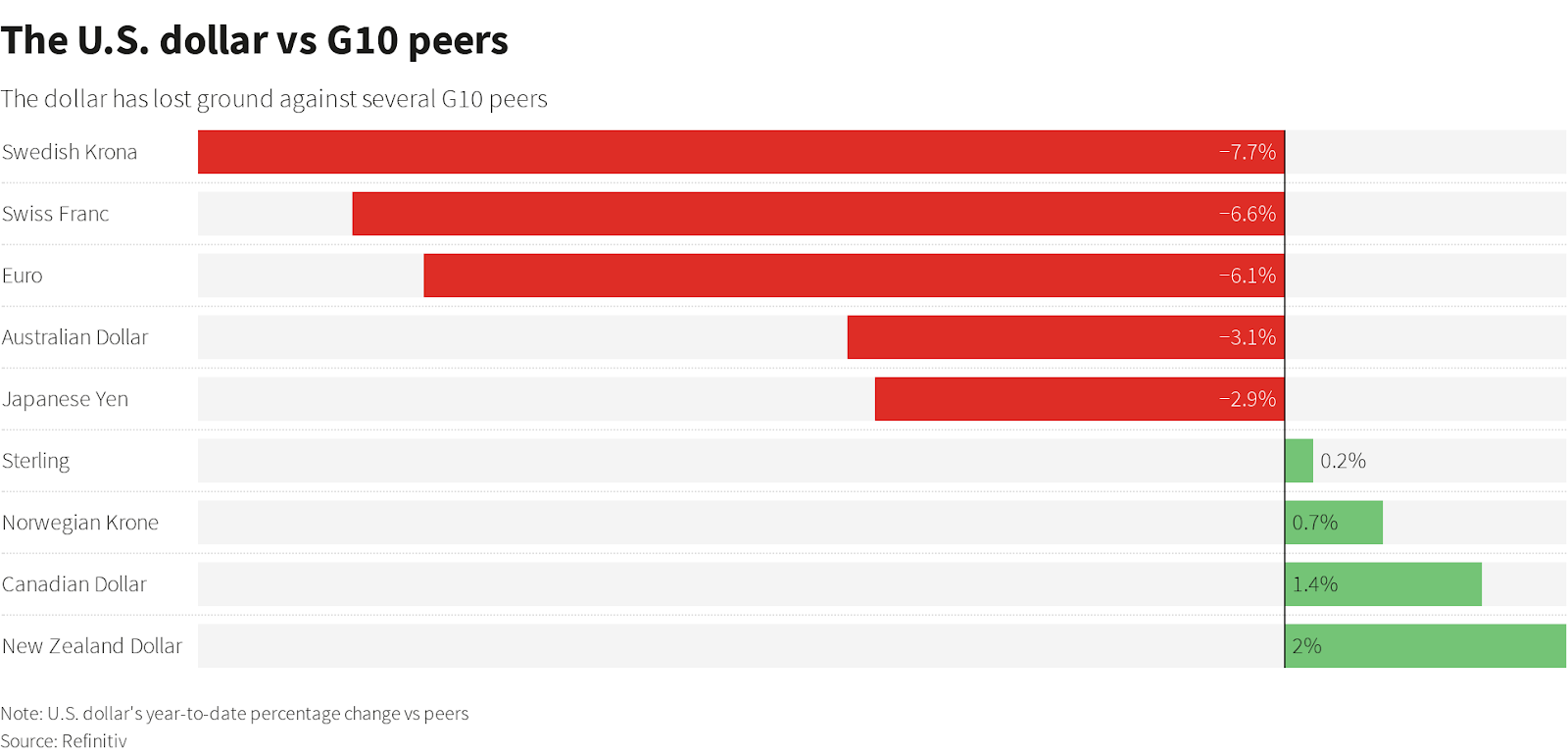

While USD has strengthened over the past week, the currency has lost ground this year against its G-10 peers. See chart below:

Weighing heavily on the broader market are:

- A comprehensive stimulus package before September remains elusive, leaving the U.S. economy on the fringe.

- The U.S.-China relations show little sign of easing, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- There is still no date scheduled to discuss the current status of the phase-one U.S.-China trade accord.

- Uncertainty and the prospect of a drawn-out and heavily litigated November presidential election.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.

- To date, globally, there have been over 23.2+ million cases and 805,000+ deaths.

- The U.S. FDA, on Sunday, fast-tracked and cleared the usage of convalescent plasma for use in certain COVID019 patients – though studies to prove its benefits and risks haven’t been completed.

Up ahead this week:

- On Tuesday, the Consumer Confidence index for August and new home sales in July data.

- Wednesday, Durable Goods orders for July and the latest EIA crude oil inventory data.

- Thursday will be heavy with Q2 GDP, initial weekly jobless claims, pending home sales, and Fed speak at the Jackson Hole virtual symposium.

- Friday will continue with the Jackson Hole economic forum and we’ll also see PCE inflation data.