Market Snapshot

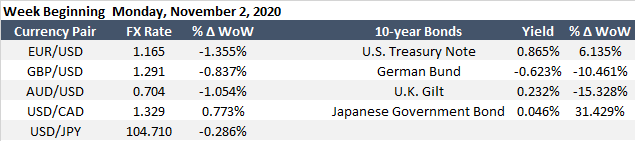

Much of the recent market volatility comes to a head this week as investors brace for tomorrow’s U.S. election, a Fed decision on Thursday, and the October employment report on Friday. USD rates extremely volatile this morning with both short-term and long-term rates fluctuating between a rise and then a fall before rising again this morning. The 10-year U.S. Treasury yield is now trading 0.0261% lower to 0.853%.

U.S. Growth Rebounds 33.1%

Last week’s third-quarter GDP print showed a 33.1% annualized rebound that was unprecedented in size, however, the economy is still 3.5% smaller than it was in the fourth quarter of last year.

- The recovery was primarily due to a 40.7% rebound in consumption, a 70.1% rebound in investments in business equipment, and residential investment increasing by 59.3%.

- Non-residential real estate investment spending fell by 14.6% in the third quarter along with government (Federal, State, and local) expenditures declining by 4.5% which will likely continue over the coming quarters unless more fiscal stimulus is provided.

Election Outcome

Investors have in recent weeks bid up long-term rates in hopes of a fiscal deal that remains elusive. Despite the near-term political uncertainty and rising COVID-19 cases in Europe and the U.S., investors remain optimistic about the economic outlook given recent economic data prints and expectations of fiscal stimulus regardless of which political party wins. The 10-year USD swap rate is currently 17bps higher from a month ago.

While the election results will likely be a catalyst for a major shift in interest rates, currencies, and equity markets, the largest immediate shift would come if the presidential election outcome is contested. A contested election would likely lead to an immediate sell-off across risk assets and demand for safe-haven assets such as U.S. Treasuries would ensue.

Fed November Meeting

The Fed will convene this week on Wednesday and Thursday (to avoid clashing with the election) to discuss monetary policy and set interest rates. Given the recent positive economic data, the Fed is unlikely to provide more accommodation and will likely be a relatively quiet meeting.

The recent rise in the 10-year U.S. Treasury yield, which has trended higher to above 0.85% from the record low of 0.50% in early August, may put the Fed on alert. While the rise is in part a reflection of rising inflation it also reflects an increase in real yields which risks an unwanted tightening in financial conditions. We will be looking for the Fed’s interpretation of risks to its outlook amid the recent spike of COVID-19 cases and potential post-election stimulus.

Weighing heavily on the broader market are:

- The U.S. November Elections

- Investors and traders are bracing for a volatile election as the ultimate Presidential and Senate winners may not be known until December, pushing out typical November hedges into December and January 2021.

- U.S. fiscal stimulus package

- A fiscal stimulus package is unlikely to occur until Q1 2021.

- We may see long-end rates push higher, on inflation expectations, should Congress agree on a $2 trillion+ fiscal stimulus plan.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- Second novel Coronavirus wave

- In a dramatic reversal in recent weeks, Europe is experiencing its second wave forcing countries to impose more strict measures including full shutdowns.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.