Market Snapshot

Concerns over a global second wave of the coronavirus reversing a return to pre-pandemic normalcy are rattling markets as the number of new cases continues to surge in Europe. While COVID-19 fatalities are lower thus far, a global “V-shaped” economic bounce back is looking increasingly unlikely. Central banks around the globe have continued their quantitative easing policies by supporting low to negative rates. U.S. Equity futures are pointing to a lower open with the S&P 500 futures down 61.45 points. WTI Crude oil is -2.41% lower to $40.12/barrel as demand breaks. A global flight-to-safety in bonds ensues as rates fall. The 10-year USD swap is 4bps lower to 0.663%.

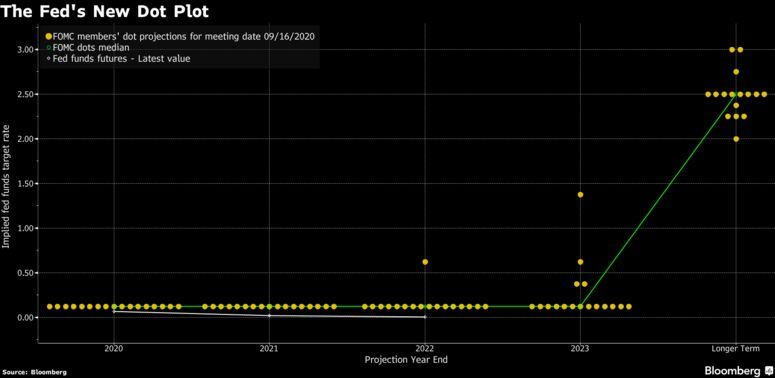

Fed Reaffirms Lower Rates Lower For Longer

The Fed, at the conclusion of its two-day meeting last week, said it expects to hold interest rates near zero until the labor market has reached maximum employment and inflation has reached 2% and is on track to moderately exceed that for some time. The committee also forecasted that rates will stay near zero at least through 2023, as shown in the Fed ‘dot plots’. The market reacted with mid to long-dated Treasuries selling-off post-Fed meeting, pushing yields higher before leveling off at the end of the week.

- The FOMC kept rates unchanged with the Fed Funds’ target range to remain between 0% and 0.25%.

- Chairman Powell highlighted that “more fiscal support is likely to be needed” as there are ”still roughly 11 million people out of work due to the pandemic.”

- Fed Chairman Powell and U.S. Treasury Secretary Mnuchin are scheduled to testify before Congress beginning Tuesday on fiscal policy amidst the coronavirus pandemic.

The 10-year U.S. Treasury Note is trading -0.034% lower to yield 0.66%.

Are Negative Rates on the Horizon in the UK?

Upon the conclusion of last Thursday’s Bank of England (BoE) meeting, the committee kept its key funding rate unchanged at 0.1%. Surprisingly, the BoE in a press statement said “it would begin structured engagement” with UK regulators on how negatives rates might work should “the outlook for inflation and (GDP) output warrant it at some point during this period of low equilibrium rates.”

Perhaps more surprising is that the thought of negative interest rates is “conditioned on the assumption of an immediate, orderly move to a comprehensive free trade agreement with the European Union (EU) on January 1, 2021.” While implementation is unlikely to occur in Q4 2020, what happens if a trade agreement doesn’t materialize? The outlook for a successful trade agreement by year’s end between the UK and EU looks increasingly unlikely after Boris Johnson introduced legislation that would defy an already agreed upon arrangement regarding the Northern Ireland trade border.

GBP/USD is 0.48% weaker at 1.296. The 10-year UK Gilt is currently trading at 0.16%.

European Central Bank to Review its Asset Purchase Program

Christine Lagarde, the European Central Bank President, has launched a review of its current asset purchase programs after expanding its bond-buying program in March to the tune of €1.35 trillion in June. The primary question is how much longer should the bank continue its Pandemic Emergency Purchase Program (PEPP) and whether the bond-buying flexibility should be merged with the greater ECB long-term quantitative easing schemes.

- Prior to the implementation of the PEPP, the ECB’s sovereign bond purchases were structured to avoid using monetary policy to directly finance governments.

- The implementation of the PEPP removed the restriction of only buying up to a ⅓ of a country’s debt and allowed the ECB to buy sovereign debt proportionally to the size of each country’s economy without regard to credit quality.

The 10-year German Bund is trading 0.039% lower to yield -0.519%.

Weighing heavily on the broader market are:

- A comprehensive stimulus package in the U.S. is unlikely to be received before October and may potentially be delayed until Q1 2021, leaving the U.S. economy on the fringe.

- We may see long-end rates push higher, on inflation expectations, should Congress agree on a $2 trillion+ fiscal stimulus plan.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- Uncertainty and the prospect of a drawn-out and heavily litigated November presidential election

- Second Coronavirus wave.

- To date, globally, there have been over 31+ million cases and over 960k deaths according to the New York Times.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.

Up ahead this week:

- Today we have Fed Chair Powell, Brainard, Kaplan, and Williams speaking.

- On Tuesday U.S. Fed Chairman Powell will testify before Congress on coronavirus economic response (CARES Act). Additionally, we will have data on existing home sales for August.

- Wednesday brings us September Manufacturing PMI as well as Crude Oil inventories. FOMC member Mester and Quarles to speak.

- Thursday brings us another round of initial jobless claims (forecast to come in at 843k) and New Home Sales for the month of August. U.S. Treasury Secretary Mnuchin to speak.

- Friday shows the Core Durable Goods orders for August along with the Baker Hughes total oil rig count. Closing out the packed week of Fed speakers will be FOMC member Williams.