Market Snapshot

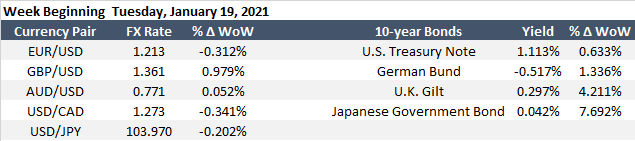

Risk is skewed towards the upside this morning, ahead of the inauguration of President-elect Joe Biden, and as of Q4 2020 U.S. corporate earnings are kicked into high gear. Former Fed Chair and incoming U.S. Secretary Treasury Janet Yellen is scheduled to speak before the Senate Finance Committee at 10 AM EST today where it is expected that she will urge Senators to “act big” in response to the coronavirus’ toll on the U.S. economy — further paving the way for big fiscal initiatives. 10-Year UST is currently +0.02% to 1.113% while 10Y USD swaps are up another 1.3bps to 1.113%.

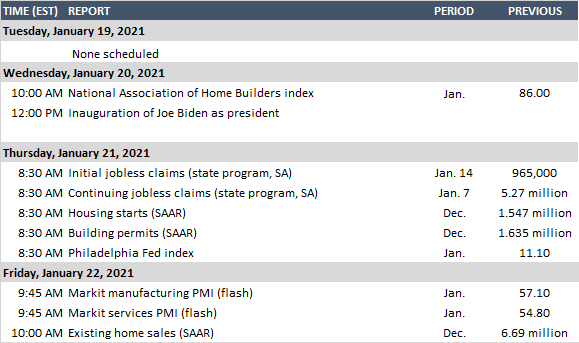

Treasury Auctions:

Jan. 19: 13-, 26-week bills; 42-, 119-day cash-management bills

Jan. 20: 20-year bonds

Jan. 21: 4-, 8-week bills; 10-year TIPS

Reflation Trade Continues

Continuing the 2020 U.S. elections theme of a Congress, Senate, and Presidency controlled by Democrats, investors have continued to sell U.S. Treasuries en masse after the recent Georgia Senate race ended in a “blue wave” win for the incoming Biden administration. U.S. 10-year Treasury yields have rallied over 20bps and broke through the 1.00% level trading as high as 1.15% last week.

With the “blue wave” came a massive proposal by the incoming Biden administration to the tune of $1.9 trillion of fiscal stimulus as part of Biden’s “first step” on the road to recovery for the coronavirus-battered U.S. economy. While $1.9 trillion may not be the final number, the idea that the incoming administration is willing to spend significantly more will be inflationary and lowers the chances that the Federal Reserve will need to provide further stimulus.

How much higher yields can run will depend on the economic recovery and may in part be further fueled by the “second step” of the Biden administration’s plans for fiscal stimulus in the form of infrastructure spending — to be announced in February. While many economists debate what’s next for yields, bond dealers such as Goldman Sachs raised their year-end target for 10-year yields to 1.5% from 1.3%, given the “greater fiscal impulse” likely under unified Democratic control of the government.

What about the Fed?

With both the U.S. Treasury and USD swap curve steepening, there has been talk amongst members of the FOMC about a premature tapering of the Fed’s $120 billion of monthly bond purchases and subsequently interest rate hikes. In response, Fed Chairman Powell last Thursday, said it is too early to begin talking about changing the central bank’s monetary policy. Powell will likely wait for “clear evidence” that employment and inflation goals are met before making any monetary policy adjustments. With the COVID-19 vaccines being rolled out and the velocity of an economic recovery to pick up in the second half of the year, Kansas City Fed President Esther George and St, Louis Fed President James Bullard have cited higher inflation as a concern. Atlanta Fed President Raphael Bostic said Monday that it might be possible for the central bank to raise rates as soon as mid-2022 backing up the assertion that price growth could accelerate sooner than Fed officials previously forecasted.