Market Snapshot

RISK-OFF sentiment. Despite Congressional leaders agreeing over the weekend on a $900 billion pandemic aid package on top of $1.4 trillion funding for government operations, U.S. equity futures and Treasury yields are trading lower this morning, as of this writing. Concerns over the weekend of a new COVID-19 strain that is spreading wildly in the United Kingdom has resulted in countries both inside and outside the European Union to close their borders and impose travel restrictions. Adding the risk-off sentiment is the rising risk of a no-deal Brexit.

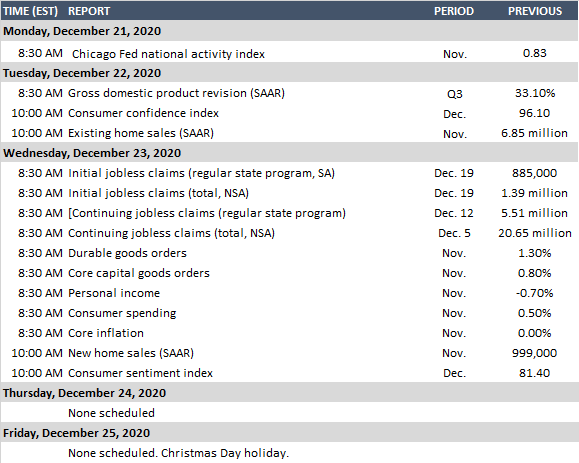

It’ll be a light data week with the Christmas holiday around the corner. Data on weekly jobless claims, home sales, and personal income are due on Wednesday.

U.S. markets are scheduled to close early at 2 PM EST on Thursday and all day on Friday.

Fed Policy Unchanged… Mostly

The FOMC concluded its two-day meeting last Wednesday and announced a small tweak to its monthly $120 billion of asset purchases. The new language implies that its current asset purchases could continue for longer than market participants expected.

After the last FOMC meeting, the Fed was willing to commit to continuing its asset purchases “over coming months” but instead will now be outcome-based rather than time-based. Interestingly, there was no mention of the recent surge of coronavirus cases or acknowledgment that vaccines should be widely available next year.

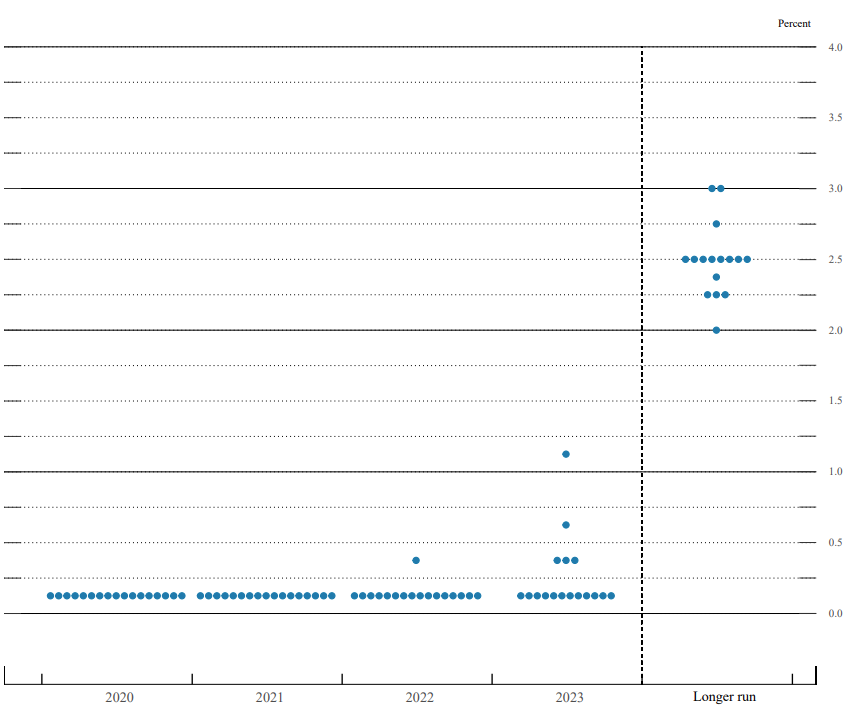

The Fed’s Dot Plot shows that officials expect no change in policy next year and borrowing costs near zero through 2023, based on median estimates. The FOMC states that monthly purchases of $120 billion in assets will continue “until substantial further progress has been made toward the FOMC’s maximum employment and price stability goals”. As “substantial progress” is vague, the 10-year U.S. Treasury yield rose 2bps post announcement.

Industrial Production Continues to Catch up with Consumption

Manufacturing output increased by a solid 0.8% in November with companies rebuilding their lean inventories. Nearly half of the 0.8% month-over-month (MoM) gains were driven by a 5.3% MoM increase in auto production — which is now back to pre-covid levels. However, excluding the auto industry, manufacturing output is still down by nearly 4%. Weighing heavily on output is the snail’s pace recovery in manufacturing of business equipment which is still down 10% YoY, though consumer production has nearly posted a full recovery. While the services secretary is expected to drop due to the new virus-related restrictions, production should continue to rebound over the coming months if not the rest of 2021.

Long Bleak Winter for Retail Sales

The recent surge in coronavirus infections has led a number of states to re-impose lockdowns and many to re-impose tougher restrictions, resulting in a worse than expected decline in November retail sales. With daily infection rates continued to increase, it’s expected that retail sales will further decline in December.

Retail sales declined by 1.1% MoM in November, although autos only fell by 1.7% MoM. Gasoline sales fell by 2.4%, MoM. Food services dropped 4.4% MoM, while grocery store sales increased by 1.9% MoM — mirroring data earlier this year when stay-at-home restrictions were in place. Electronics and clothing sales fell by 3.5% and 6.8%, respectively, indicating that Black Friday and Cyber Monday sales were disappointing this year. Softness in spending will likely lead to a weaker Q4 2020 GDP print, though the economy will likely bounce back strongly by Q2 2021 as vaccine deployment reaches critical mass in the U.S.

No Deal Brexit Looming Over Fishing Rights

The British Pound took a beating today as the UK and EU are deadlocked on Brexit trade talks while a new strain of COVID-19 was identified over the weekend. With the revised deadline of December 31 around the corner, the two sides are deadlocked on a few key matters:

- The EU is worried the UK could provide financial aid or incentives to home companies to which it deems an unfair advantage

- Both sides are concerned about who will be allowed to fish in UK waters

- Both sides are unable to agree on enforcement policies

- While there has been some compromise over the Northern Ireland border, there is still a dispute over border control checks and tariffs.

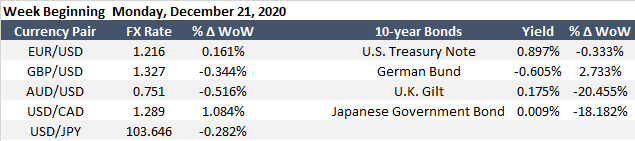

The Cable is currently trading at 1.3287.

Weighing heavily on the broader market are:

- U.S. fiscal stimulus package

- A nearly $900 billion fiscal-aid package is scheduled to vote later today.

- Should the significantly smaller fiscal stimulus package fail to pass, we will unlikely see a revisit until late Q1 2021.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- The Trump administration banned investments in companies controlled or owned by China’s military. Current investors will have until November 11, 2021, to comply with the ruling that goes into effect on January 11, 2021.

- Adding to the list of banned companies are now Chinese chipmaker SMIC and drone manufacturer DJI Technology, amongst others.

- Relations will unlikely thaw under the Biden administration as Biden has stated he would not make “any immediate moves” to scrap the 25% tariffs on China — though he has emphasized his commitment to a multilateral approach

- Coronavirus

- The U.S. FDA has formally approved the Pfizer/BioNTech (over 90% effective) and Moderna (over 95% effective) vaccines in a major turning point in humanity’s battle against COVID-19.

- A new and highly contagious strain of the Coronavirus has been reported in the UK though we do not yet know if it is more deadly. The efficacy of the two approved vaccines is also currently unknown.

- Meanwhile, the number of COVID-19 cases continues to rise and hospitals across the country are in various stages of being at or near capacity.

- While there are numerous COVID-19 vaccines and therapeutics on the horizon, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out towards the end of 2021.