Market Snapshot

Investor optimism rises after the U.S. and China held a phone call last Tuesday about the implementation of the phase-one trade agreement. Additionally, as the economy continues its K-shaped recovery and re-emerges from the virus shutdowns earlier this year, U.S. equity futures point to another higher open after setting fresh record highs last Friday. Dow futures are +0.10%, S&P 500 futures are +0.22%, and NASDAQ futures are +0.42%.

Meanwhile, while short-term funding rates in the U.S. remain low (Fed Funds rate is currently 0.08%), the U.S. Treasury yield curve has steepened with the 2s10s spread now over 60bps. A year ago, the yield curve inverted and the 2s10s spread turned negative, indicating a looming recession which we have now experienced.

With hurricane Laura in the rearview mirror, WTI crude oil prices are 1.21% higher to 43.485 per barrel on the back of stronger demand and lower production. Gold spot rates remain elevated at 1,967.

Fed Tweaks Policy

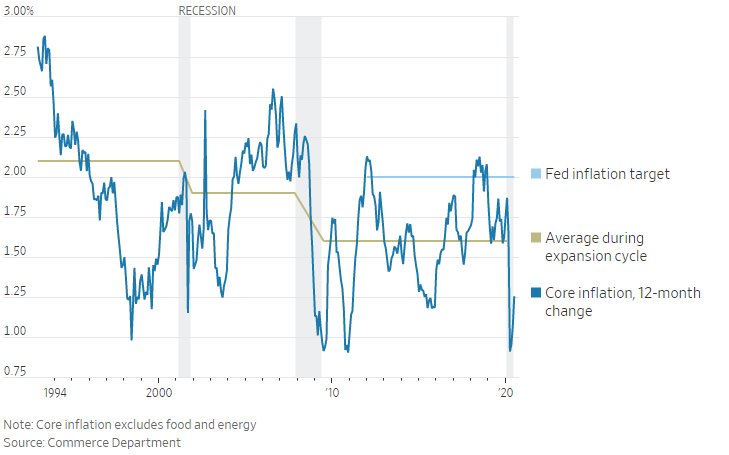

Last Thursday, during the Jackson Hole Symposium, Federal Reserve Chairman Jerome Powell announced a significant policy shift in how it sets interest rates by dropping its longstanding practice of raising interest rates to obviate higher inflation. The revamped policy-setting framework will now allow inflation to rise modestly, on average, above its 2% target. The time-frame for calculating the average was not defined.

The change is to address the “reality of a quite difficult macroeconomic context of low-interest rates, low inflation, relatively low productivity, slow growth, and those kinds of things.” Realized core inflation vs. the Fed’s 2% target (see image below):

Age Is Just a Number

On Warren Buffet’s 90th birthday, Berkshire Hathaway Inc. disclosed its long-term investments in each of the five leading Japanese trading conglomerates. The investments were made through regular purchases on the Tokyo Stock Exchange over a 12-month period. The current stakes equate to 5% of each company with the option to increase its holdings up to a maximum of 9.9%. The five conglomerates are Itochu Corp., Marubeni Corp., Mitsubishi Corp., Mitsui & Co., and Sumitomo Corp. The Nikkei 225 closed 1.12% higher to 23,140, outperforming is peers in Asia.

The Japanese Yen fell against the U.S. Dollar (105.90) after Japan’s longest-serving Prime Minister, Shinzo Abe, confirmed his intention to step down due to worsening health. His resignation will be in effect after the ruling Liberal Democratic Party formally appoints a new leader. It is highly expected that the successor will continue “Abenomics” policies of fiscal, monetary support, and economic reforms.

The 10-year Japanese Government Bond (JGB) traded -0.011% lower to a yield of 0.046%. The U.S. Treasury yield, by comparison, is 0.733% while the 10-year German BUND yield is -0.385% as of this writing.

The Dow Reshuffle

The first reshuffling of companies in the Dow Jones Industrial Average (DJIA) since 2013 comes on the heels of technology company Apple’s 4-for-1 stock split. Oil giant Exxon Mobil (XOM), drugmaker Pfizer (PFE), and defense contractor Raytheon Technologies (RTX) will be replaced by the cloud-based customer relationship management software company Salesforce.com (CRM), the biotech firm Amgen (AMGN), and the industrial conglomerate Honeywell (HON).

Of interest will be the change to the ‘divisor’ or the number that is used to determine the influence of the 30 companies that make up the price-weighted index. The new divisor is likely to be 0.152 which translates to a swing of 6.579 points per $1 price move.

USD Mean Reversal

After a temporary USD rebound, traders returned to the crowded short USD trade. With USD funding rates already near 0%, the Federal Reserve’s plan to allow for low-interest rates for longer continues to push the USD lower. With uncertainty over the upcoming U.S. November presidential election, investors bet on a EUR/USD increase to $1.25 after the U.S. elections.

Supporting the EUR currency has been the European Union’s policy response to the coronavirus compared to the United States and its expected trajectory of economic recovery. The Euro is up another 0.23% against the U.S. Dollar to 1.193.

- While the USD has historically gained after Presidential elections, a win for Joe Biden (the current leader in polls) could hurt the currency as the Democratic nominee has called for an increase in taxes on wealthier Americans and increasing federal spending.

- Link to polls data: https://realclearpolitics.com./epolls/2020/president/us/general_election_trump_vs_biden-6247.html

Weighing heavily on the broader market are:

- A comprehensive stimulus package in the U.S. is unlikely to be received before October, though a deal could be made in September, leaving the U.S. economy on the fringe.

- The U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- In a piece of surprisingly positive news, representatives from both countries met last Tuesday to discuss phase-one of the trade agreement.

- Uncertainty and the prospect of a drawn-out and heavily litigated November presidential election.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.

- To date, globally, there have been over 25.2+ million cases and nearly 846,000 deaths.

Up ahead this week:

- On Tuesday, its monetary policy decision day at the Reserve Bank of Australia along with ISM manufacturing data in the U.S.

- Wednesday will have Australia’s GDP print.

- Thursday we will receive additional data on Initial weekly jobless claims for the week ending August 29.

- Friday brings the August U.S. jobs report. Current forecasts show payrolls continued to rebound in the month of August.