RISK-ON investor sentiment continues as U.S. equity futures advance higher alongside European and Asian equities. U.S. Treasury prices fell while yields continue to climb. The 10-year U.S. Treasuries are currently trading 2.6bps higher to 1.776%.

Investor optimism reverberated through the global markets last week as a trifecta of positive headlines including the U.S.-China agreement to a phase-one trade deal, the UK and EU agreement on Brexit, and a strong kick-off to corporate bank earnings. The resulting optimism led to a steepening of the U.S. Treasury yield curve (the spread between 2-year and 10-year yields are now 5.5bps wider to 17.5bps). While fears of an economic downturn have eased this month, an unraveling of the U.S.-China “mini-deal” or a no-deal Brexit could quickly send bond yields to its September lows.

U.S.-China Trade War

- China and the U.S. “agreed in principle” to a “mini-deal” on October 11, the first major breakthrough in the 18-month trade war. The highlights are as follows:

- China will purchase up to $50 billion in U.S. agricultural goods.

- The U.S. purchased approximately $9 billion in 2018, down from $25.8bn in 2012.

- China will boost intellectual protection, primarily for small and medium businesses.

- China will commit to currency changes.

- The agreement over currency will likely mirror commitments already made with the International Monetary Fund (IMF) standards.

- The U.S. will suspend additional tariffs.

- Tariffs on $250 billion of Chinese goods were supposed to go into effect last Tuesday, October 15.

- China will purchase up to $50 billion in U.S. agricultural goods.

- Both parties will continue lower-level talks to work out the details this week before it is to be signed by Trump and Chinese President Xi at the Asian-Pacific leaders’ summit in Chile on November 16-17.

Other U.S. Trade Wars

- October 18 – After the U.S. won a case against the EU’s subsidies to Airbus, the U.S., on Friday, imposed $7.5 billion in tariffs on goods originating from the European Union.

- November 14 – Trump will need to decide if he will go through with placing 25% tariffs on imported autos and auto parts.

- Q4 2019 – NAFTA 2.0 – The triparty trade agreement between the United States, Mexico, and Canada is still in process of being finalized with a target date of the end of October so that Congress can vote before year-end.

UK-EU Brexit Agreement

- Global markets rejoiced last week when the current Prime Minister, Boris Johnson, agreed to a Brexit deal with the European Union (a three-year saga).

- Unsurprisingly, Johnson was defeated over the weekend when the U.K. Parliament voted to delay the Brexit decision.

- The dramatic vote left Johnson furious as he told Parliament he will not reach out to the EU to extend the October 31 deadline (which would be unlawful).

- While Johnson eventually agreed to ask the EU for an extension, he will try again to put his proposal to the test today in the House of Commons.

- As there is increasingly more clarity over Brexit, U.K. equities, bonds, and real assets become more attractive to investors.

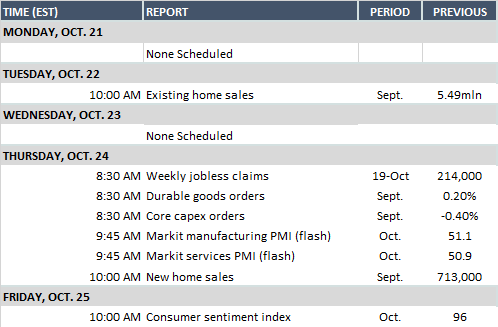

The Fed and Economic Data

- The Fed is in blackout mode before next week’s FOMC meeting (Oct. 29-30).

- Fed Funds futures are pricing in a rate cut after Vice Chairman Richard Clarida’s comments last Friday regarding the central bank will “act as appropriate” to sustain the expansion as risks remain “evident”.