Strong investor sentiment continues after the world’s two biggest economies are close to finalizing parts of the phase one trade deal. Both President Trump and Xi plan to sign the initial deal at the Asian-Pacific leaders’ summit in Chile next month on November 16-17. Last week, investor optimism pushed the S&P 500 briefly to an all-time high, over the past three months, closing at 3022.55. Crude oil had its biggest weekly gain in more than a month as supplies continue to tighten amongst strong demand. West Texas Intermediate (WTI) crude oil closed the week at $56.66 per barrel. The 10-year U.S. Treasury closed nearly 5bps higher at 1.798% and is opening nearly 4bps higher at 1.83% this morning.

U.S.-China Trade War

- China confirmed over the weekend that parts of the text for the initial phase of the trade deal with the U.S. are “basically completed”, echoing the U.S. Both parties will continue lower-level talks to work out the details before it is to be signed by Trump and Chinese President Xi at the Asian-Pacific leaders’ summit in Chile on November 16-17.

- China and the U.S. “agreed in principle” to a “mini-deal” back on October 11, the first major breakthrough in the 18-month trade war. The highlights are as follows:

- China will purchase up to $50 billion in U.S. agricultural goods.

- The U.S. purchased approximately $9 billion in 2018, down from $25.8bn in 2012.

- China will boost intellectual protection, primarily for small and medium businesses.

- China will commit to currency changes.

- The agreement over currency will likely mirror commitments already made with the International Monetary Fund (IMF) standards.

- The U.S. will suspend additional tariffs.

- Tariffs on $250 billion of Chinese goods were supposed to go into effect last Tuesday, October 15.

- China will purchase up to $50 billion in U.S. agricultural goods.

Other U.S. Trade Wars

- October 18 – After the U.S. won a case against the EU’s subsidies to Airbus, the U.S. imposed $7.5 billion tariffs on goods originating from the European Union.

- November 14 – Trump will need to decide if he will go through with placing 25% tariffs on imported autos and auto parts.

- Q4 2019 – NAFTA 2.0 – The triparty trade agreement between the United States, Mexico, and Canada is still in process of being finalized with a target date of the end of October so that Congress can vote before year-end.

UK-EU Brexit Agreement

- UK Prime Minister, Boris Johnson, won the first-ever majority in the House of Commons for a Brexit withdrawal agreement.

- The joy was short-lived as lawmakers in the UK are rejecting Boris Johnson’s push for an early election (in another attempt to receive a two-thirds vote in the House of Commons to achieve Brexit this Thursday, October 31).

- A vote for a December 9 snap election will occur today.

- In advance of the UK’s vote for an early election, France, on Friday, blocked the EU’s attempt to delay Brexit for another three months. France, however, capitulated this morning and is considering another delay of up to three months. The Cable (GBP/USD) is trading higher on the news to 1.28323. The Euro/British Pound cross is also trading higher at 0.86483.

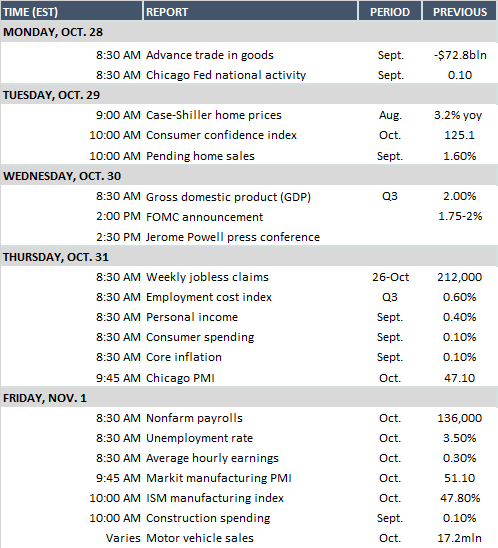

The Fed and Economic Data

- FOMC meeting (Oct. 29-30).

- Fed Funds futures are pricing in a 25bps rate cut to a target range of 1.50% – 1.75%.

- Fed Funds futures for the December contract have trimmed down the odds of a cut from near certainty to less than 32%.

- Question will be whether this is the final cut for the Fed or will they continue as “appropriate”?

- While rare, if the Fed does not cut interest rates as the market expects, we expect to see equities and bond prices sell-off.

Key events coming up this week:

- Corporate earnings season is well underway with the following large companies reporting: HSBC (disappointing earnings released earlier this morning), Alphabet, Facebook, Pfizer, Airbus, Apple, Exxon Mobil, BP, PetroChina, Credit Suisse, Nomura and Macquarie Group.

- On Wednesday, the Fed’s interest rate decision is due. Fed Funds futures are currently pricing in a 25 basis point cut. The U.S. GDP data will also report with economic growth forecast to have slowed to 1.6% in Q3 2019 (the slowest pace this year).

- The Bank of Canada will also set its rate policy.

- On Thursday, the Bank of Japan sets its rate policy and will hold a news conference post-meeting.

- On Friday, we will have the monthly jobs report. Economists forecast only an 88,000 increase in jobs created for the month of October. If met, this would be well below the prior month’s 136,000 gain.