Investors, recently, have a multitude of reasons to be optimistic as a majority of corporate earnings continue to beat analyst’s expectations. Further fueling equity and debt growth, the Fed cut its key target interest rate by 25 basis points to an upper target of 1.75%. A strong print in the U.S. employment and consumer spending report last week and positive movement in the U.S.-China trade negotiations pushed U.S. equity indices to new highs with the S&P 500 closing at 3,066.91. The 10-year U.S. Treasury note closed the week at 1.717% and the USD swap curve continues to be inverted (though is steepening) with the 1year swap trading at 1.714% and the 5-year swap trading at 1.543%.

U.S.-China Trade War

- As if there were not enough “bumps in the road”, Chile canceled the Asian-Pacific leaders’ summit (APEC), which was original to be held next week on November 16-17 citing concerns over community affairs.

- Over the weekend, both the U.S. and China confirmed that the cancellation of the APEC summit would not prevent both sides from finalizing and signing ‘phase 1’ of the trade deal.

- The U.S. Commerce Secretary, Wilbur Ross, met with China Premier Li Keqiang and reported that both sides are “very far along” with ‘phase 1’ of the deal negotiations. He was “quite optimistic” that all remaining items would be resolved.

- On Friday, China reported that both sides had reached “consensus on principles” and discussed the “next consultations arrangements”.

- The highlights of the October 11 mini-deal principles are as follows:

- China will purchase up to $50billion in U.S. agricultural goods.

- The U.S. purchased approximately $9 billion in 2018, down from $25.8bn in 2012.

- China will boost intellectual protection, primarily for small and medium businesses.

- China will commit to currency changes.

- The agreement over currency will likely mirror commitments already made with the International Monetary Fund (IMF) standards.

- The U.S. will suspend additional tariffs.

- Tariffs on $250 billion of Chinese goods were supposed to go into effect last Tuesday, October 15.

- China will purchase up to $50billion in U.S. agricultural goods.

The Fed and Economic Data

- The FOMC met last Tuesday and Wednesday, October 29-30, and decided to cut the Fed Funds target rate by 25bps.

- Fed Funds futures for the December contract have further trimmed down the odds of a cut from near certainty to less than 26%, down 6% from a week ago.

- The Fed has positioned itself that no more rate cuts or hikes will occur until PCE inflation reach its target of 2%.

- Non-Farm Payrolls rose by +128,000 in October, exceeding an estimate of +75,000 from economists.

- August employment data was revised from +168,000 to +219,000.

- September employment data was revised from +136,000 to 180,000.

- The unemployment rate ticked slightly higher from 3.5% to 3.6%, near a 50-year low.

- The average pace of hourly earnings increased slightly by 0.1% to an annualized 3% gain.

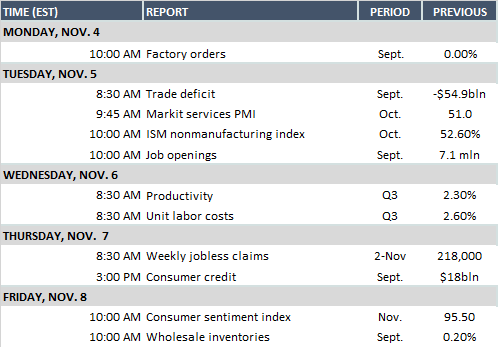

Key events coming up this week:

- Corporate earnings season is well underway with the following large companies reporting: Uber Technologies Inc., Shake Shack Inc., and Hertz Global Holdings Inc. to report this week.

- The final September reading for U.S. factory and durable goods orders will be published at 10 AM EST.

- San Francisco Fed President, Mary Daly, speaks in New York today.

- The new European Central Bank President, Christine Lagarde, will give her first speech in Berlin, Germany’s capital.