Since January, when the early cases of the novel coronavirus (COVID-19) were alerted to the world, investors had hoped for a quick V-shaped recovery in risk assets as had occurred in 2003 following the SARS epidemic. For nearly two months, the virus appeared contained within the borders of China with 35.18% of patients discharged from the hospital a week ago. All bets were on a similar 2003 recovery. However, in a matter of a few days, those hopes were thwarted as the coronavirus suddenly spread outside the Asian continent to Europe in Northern Italy. Here in the U.S., the Centers for Disease Control (CDC) announced last Tuesday that the virus was coming to the U.S. and for people to prepare.

In response, risk assets around the globe sold off with a vengeance. The S&P 500 equity index was down as much as nearly 12% at its worst for the week. U.S Treasuries were heavily bid as the global demand for flight-to-safety securities continued. The yield on the 10-year U.S. Treasury Note fell to 1.073% from 1.37%, a 29.7bps drop.

While Federal Reserve officials were initially unnerved by the economic impact from the coronavirus, Fed Chairman Powell made a rare statement 90-minutes before the market close last Friday pledging to “act as appropriate” to support the economy. The statement opens the door for a rate cut at its next meeting, on March 17-18. While there is no doubt that a rate cut(s) will have limited impact amidst a global health emergency that threatens to reduce both supply and demand in the U.S. economy, it will certainly provide some relief/fuel to those that are heavily leveraged.

During Asia trading hours, following China, Italy, and the Fed’s stated efforts to boost their respective economies, the Bank of Japan pledged to inject liquidity and increase asset purchases. When the UK opened for trading, the Bank of England said it will take steps to protect the stability of the economy. It is widely expected that the Group of Seven (G7) finance ministers will coordinate a response. The G7 includes countries from Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

Investors welcomed the global concerted efforts to counter the negative economic impact from the coronavirus and boost the economy. The S&P 500 futures point to a 0.80% gain at the open, as of this writing. Equities initially sold off across the globe after China’s official manufacturing purchasing managers’ index at the weekend showed factory activity plunged to an all-time low in February, due to the coronavirus. USD rates continue to be depressed as bond investors continue to pour money into U.S. Government securities (bond prices have an inverse relationship to yields.)

What’s Next?

The number of confirmed cases in China has since slowed to an average of 411 new cases over the past week with 55.56% of patients now discharged. Factories have restarted and the Chinese government has pledged support to a wide array of businesses.

While China appears to be on its way to recovery, other countries around the world are now dealing with the spread of the coronavirus. Certainly, investors welcome central bank intervention (specifically monetary policy loosening), governments will need to do its part and provide fiscal stimulus, supporting both the supply and demand-side economy. What is key will be how governments react to the spread of the coronavirus. A full shutdown, similar to that of China, will cause a greater negative impact on the global economy than the virus itself will.

Schedule of Fed Speakers (before the blackout period):

Tuesday, March 3: Cleveland Fed President Loretta Mester; New York Fed official Lorie Logan; Chicago Fed’s Charles Evans.

Wednesday, March 4: Beige Book released; St. Louis Fed’s James Bullard.

Thursday, March 5: Dallas Fed’s Robert Kaplan; Minneapolis Fed’s Neel Kashkari; New York Fed’s John Williams.

Friday, March 6: Evans, Mester, Bullard, Williams, Boston Fed’s Eric Rosengren and Kansas City Fed’s Esther George at the Shadow Open Market Committee.

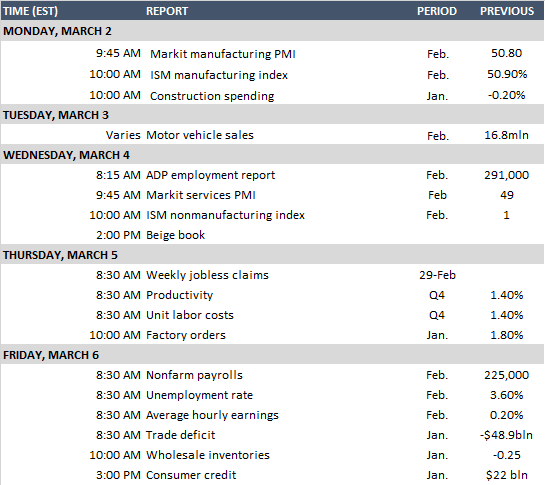

Key events coming up this week:

- Investors will continue to monitor the economic fallout from the global spread of the coronavirus.

- Markit U.S. manufacturing PMI and ISM manufacturing index, both key factory gauges, is due out on Monday. It is projected to show that U.S. manufacturing came close to stagnating in February.

- Britain and the EU will begin to negotiate their trade and various policies.

- The Reserve Bank of Australia sets its monetary policy on Tuesday.

- U.S. citizens in states including California and Texas will vote on “Super Tuesday” for the Democratic Primaries.

- The Bank of Canada will vote on monetary policy on Wednesday.

- OPEC ministers gather in Vienna on Thursday.

- Friday brings us the February U.S. non-farm jobs report.