The volatility theme continues in the capital markets on the back of the domestic political turmoil ignited last week by a whistleblower’s report involving President Trump’s communication with the Ukrainian President. The U.S.-China trade negotiations took a new turn on Friday as rumors that the White House is actively seeking to curb U.S. investments in China – dragging rates and equity indices lower to close out the week. However, White House trade adviser Peter Navarro earlier this morning stated such news as ‘fake news’. Markets are reacting positively on the news with the U.S. 10-year Treasury trading +0.02% to 1.704% and USD 10-year swaps +0.026% to 1.60%.

The outlook for U.S. GDP growth remains solid, supported by strong labor market conditions, gains in real income, strong consumer sentiment, and favorable financial conditions (particularly, lower interest rates). Last Friday, data showed that U.S. core personal consumption expenditures (PCE) through August was +1.77% YoY, its highest level since January 2019 (the Fed’s annual target rate is 2%). The economy grew at a 2.0% annualized rate last quarter, slowing from the January-March quarter’s brisk 3.1% pace.

Personal income rose 0.4% in August after nudging up 0.1% in the prior month. Wages increased by 0.6% (outpacing spending). Savings rose to $1.35 trillion from $1.29 trillion in July.

The Fed

- Vice-Chairman Clarida reinforced expectations that the FOMC will discuss additional policy accommodation soon while others push for the Fed to hold firm.

- Market forecasts a 25bps rate cut in December, should the Fed decide to cut interest rates again.

- The Fed has continued to engage in overnight and other short-term repo operations to calm conditions in the short-term funding market as volatility continues.

- Repo rates traded as high as 5.25% on September 17.

- SOFR, the secured overnight financing rate, the frontrunner to replace the USD LIBOR index, is based on the repo rate.

- The Federal Reserve is expected to discuss a long-term fix at the October meeting.

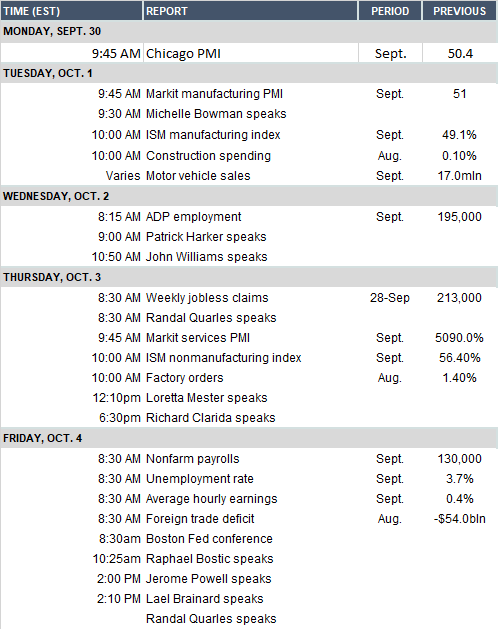

Key data releases this week:

- Tuesday: The Institute for Supply Management (ISM) publishes at 10 a.m. EST its monthly reading on U.S. manufacturing activity. A reading of 50 is the cutoff between expansion and contraction.

- Wednesday: Automatic Data Processing (ADP), produces a sneak peek at U.S. private-sector hiring two days before the official BLS jobs report. Economists expect the data to show +138,000 positions were filled in September, consistent with forecasts for another solid month for job growth.

- Thursday: ISM releases its nonmanufacturing indicator at 10 a.m. EST, providing a window into U.S. services activity in September. Economists expect the index to remain solidly in expansion, though falling slightly to 55.2 from 56.4 in August. That would be good news at a time when a pre-eminent fear among economists is that factory weakness may spill over into the much larger services sector.

- Friday: The U.S. Labor Department releases its September jobs report. With the U.S.-China trade war and the slowdown in Europe weighing on exports, manufacturing and business investment, consumers have been the sturdiest pillar supporting economic growth in the U.S. this year. Economists are forecasting nonfarm payrolls +140,000, the unemployment rate steady at 3.7%, and average hourly wages +3.3% YoY. Any sign of weakness could bode poorly for household spending, especially as consumers face the effects of higher tariffs on imported goods from China in the coming months.