A crude oil processing plant in Saudi Arabia was attacked on Saturday disrupting global oil supply. U.S. President Trump publicly condemned the attack and responded that the U.S. is “locked and loaded” and ready to respond to the attacks. U.S. officials also claim the evidence pointed to Iranian involvement heightening geopolitical risk sending crude futures higher and investors back into safe-haven assets.

Brent crude oil is trading 8.59% higher to $65.39/bbl, and WTI crude oil is 8.19% higher to $59.335/bbl. The increase in oil prices is unlikely to reverse global monetary policy easing. Following the report, the 10-year U.S. Treasury yield is trading 5.7bps lower to 1.73%.

Markets ended last week on a high note as U.S. equities reapproached its recent highs and 10-year USD swaps increased 44.6bps to 1.786%, since the beginning of September. The recent change in investor sentiment comes after the idea of a hard, no-deal Brexit fade and Sino-U.S. relations thaw. While headline Chinese industrial output data this morning show the economy slowing, the country still saw a 4.4% year-over-year increase. A trade deal with the U.S. is unlikely to change the trajectory of the Chinese economy as there are structural and debt-laden issues to grapple with. We caution that a near term Brexit deal and a trade detente between the U.S. and China is unlikely. The Trump administration is unlikely to give up significant IP enforcement and protection, and likewise, the Xi administration is unlikely to give any significant concessions until the 2020 U.S. elections.

We expect increased market volatility and trading activity on Wednesday and Friday as the quarterly IMM rolls for swaps commence, and the expiration of options and futures on cash equities and indices occur on Friday.

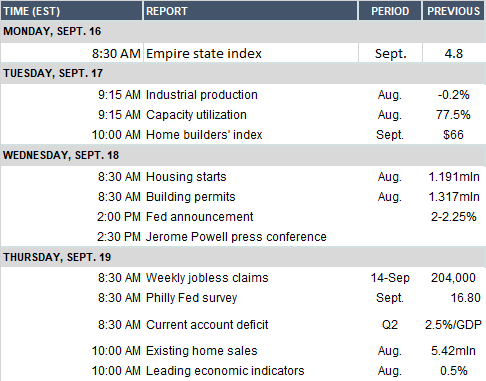

On Wednesday, the Federal Reserve will conclude its two-day meeting and is expected to lower interest rates by 25bps in response to slowing global economic growth and soft U.S. inflation. Of particular interest will be the post-meeting conference and the “dot plot” or median interest rate projections.

The Bank of England (BoE) and Bank of Japan’s (BoJ) rate decision and briefing will follow on Thursday in conjunction with employment data coming out of Australia.

See U.S. data release schedule below: