RISK-OFF – Rates and Equities are opening sharply lower this morning as the trade war between the two largest economies intensified. Last Thursday, President Donald Trump tweeted that a 10% tariff would be imposed on $300 billion worth of Chinese goods, effective September 1. Trump later said he would consider reversing course if China agreed to buy more U.S. agricultural exports. Beijing suggested it would instead take countermeasures if the U.S. tariffs were implemented.

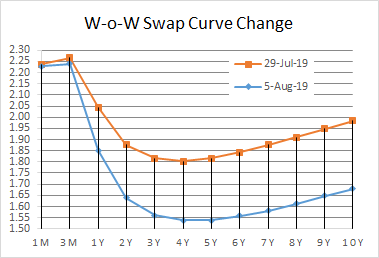

In response to the tariff threat, China allowed the USD to strengthen against the RMB and breached the Rmb7 floor. While China has likely determined that working out a deal with the U.S. is unlikely to occur in the near term and is preparing for weaker growth, we believe that a resolution could occur as driven by the 2020 U.S. election and the need to help farmers in key swing states. The 10-year U.S. Treasury yield is down nearly 30bps from a week ago to 1.77%. 10-year USD swaps are over 30bps lower to 1.67%.

For additional insight, see the BMA Market Rate Sheets.

Last week, for the first time since the Great Recession, the Federal Reserve cut its target Fed Funds rate, the U.S. interbank interest rate, to a 2%-2.25% range. To say there are strong opinions from investors and economists, for and against the decision, is to understate. On one hand, the economy is already doing what it is supposed to be doing: creating jobs and generating just enough inflation to stimulate reinvestment. On the other hand, this historically long-running expansion — which has seen quite an aggressive schedule of rate increases lately — is flashing signs of slowing. During the expansion of the 1990s, the Fed cut rates under comparable conditions with results that were at least short-term positive.

Largely lost in the noise around the rate cuts was one key sentence from the FOMC’s official release: “The Committee will conclude the reduction of its aggregate securities holdings in the System Open Market Account in August, two months earlier than previously indicated.” In other words, quantitative tightening has ended. This could turbocharge the expansionary effect of cheaper money.

Each of the three major U.S. equity indices last week dipped beneath its 50-day moving average, a widely followed technical indicator. Specifically, the S&P 500 and Nasdaq Composite dropped 3.1% to 2,632.05 and 3.9% to 8,004.07 this week, respectively, their worst performances year-to-date. The Dow Jones Industrial Average had its second-worst week of the year, sliding 2.6% to 26,485.01.

U.S. Treasury yields declined markedly during the week. Shortly after the end of the trading day Friday, the benchmark 10-year note yield fell to 1.867%, having bounced off its lowest level since November 2016. The yield on the 30-year bond dropped to 2.406%. The 2-year and 10-year spread drifted 7bps lower to 14bps. A negative spread is indicative of a looming economic recession.

Nothing like a trade war between the world’s two largest economies to spur the gold market. The London spot price was up 0.8% early Monday, at $1,451.37, a six-year high. U.S. West Texas Intermediate crude ultimately settled at $55.66 per barrel after a roller coaster ride that saw prices plummet nearly 8% before recovering 3.2% on news that oil supplies in the Middle East may be disrupted.

There are two events that have kept economic forecasters awake at night for the past couple years, and they are not going away this week: the growing trade tensions between the U.S. and China, and the ugly divorce between Britain and the European Union. If one were to be resolved over the next seven days, let us hope that it is the U.S.-China trade war. There is a deal to be had at that table. But a quick solution to the Brexit issue is more likely to lead to the third British government in as many years, and quite possibly the last. Even if that sounds far-fetched — it really is not — it could trigger recessions on both sides of the English Channel.

I. U.S. Economic Data/Markets

- Employers added 164,000 jobs in July, while wages rose 3.2% year-over-year. Job growth was slightly below forecasts, wage growth slightly above. According to ADP, 156,000 of those new jobs were in the private sector, split down the middle between large firms and small- to medium-sized firms.

- Congress passed a two-year bipartisan budget bill which essentially eliminated the debt ceiling.

- U.S. factory orders rose 0.6% in June following two consecutive declines, according to the Commerce Department.

- Consumer spending gained 0.3% despite weakness in the motor vehicle segment. This was accompanied by a 0.4% rise in personal income.

- Home prices rose an annualized 3.4% in May according to the S&P CoreLogic Case-Shiller home price indices. The rise was not experienced evenly in all cities, but declining mortgage rates tend to spur demand and keep upward pressure on home prices nationwide.

- The Conference Board’s consumer confidence index rebounded to 135.7 in July from 124.3 in June. This result far exceeded expectations.

- The Institute for Supply Management’s index of national factory activity slipped to 51.2 in July, the lowest reading in almost three years and its fourth straight monthly decline. Although this indicates a slowing of manufacturing growth, any reading over 50 still signals expansion.

II. Economics Outside the U.S.

- Chinese Economy

- Caixin/Markit’s July manufacturing purchasing managers’ index reached a better-than-expected 49.9. June’s reading was at 49.4. Still, the metric has now been below 50 for two consecutive months, indicating a contraction in manufacturing activity.

- Eurozone Economy

- Gross domestic product of the 19-member eurozone grew by 0.2% in the second quarter, according to Eurostat.

- The Economic Sentiment Indicator declined from 103.3 to 102.7 in July.

- Unemployment dropped to 6.3% in June, a record low for the Eurozone.

- German retail sales jumped 3.5% in June after a 1.7% drop in May, the largest monthly increase since 2006.

- U.K. Economy

- Due to the increasingly likely prospect of a no-deal Brexit, the pound keeps losing luster by all measures. Early Monday, it was worth $1.2112, its lowest exchange rate against the greenback in about two years, which means it is fast approaching its lowest point ever. It is also trading near a 10-year low against the euro and the yen. Eurozone inflation, however, has attenuated some of the damage compared to the euro.

- Prime Minister Boris Johnson, with less than two weeks to his tenure, has lost all margin for political error as a by-election in Wales cost him a Conservative vote in Parliament. The Tories now hold a bare, one-member majority. While many predict that his term will be a short one that ends in a no-confidence vote, some speculate that this actually might signal the dissolution of the United Kingdom of Great Britain and Northern Ireland over the issue of the Irish backstop.

- The Bank of England left interest rates unchanged at 0.75% and forecast British economic growth at 1.3% this year, down from a previous projection of 1.5%. The Bank’s 2020 outlook is for 1.3% growth, down from a previous projection of 1.6%.

- Canadian Economy

- The Dominion’s trade surplus narrowed in June to C$136 million (US$103 million), as both exports and imports dropped, Statistics Canada reports, primarily due to decreases in crude oil and aircraft trade.

- Japanese Economy

- Employment increased to 60.8% in June from 60.7% in May.

- Industrial production decreased by 4.1% in June on a year-over-year basis.

- The consumer confidence index declined to its lowest level in more than five years in July to 37.8, following the previous month’s record low of 38.7.

- Construction orders fell 4.2% on a yearly basis in June, on top of the previous month’s 16.9% decline.

- Housing starts climbed 0.3% on an annual basis in June, defying expectations of a 2.2% fall.

Key data/events this week:

- Monday

- Fed Governor Lael Brainard speech

- U.S. PMI

- Eurozone PMI

- U.K. vehicle sales

- Japan household spending

- Japan average cash earnings

- Tuesday

- St. Louis Fed President (James Bullard) speech

- U.S. economic optimism

- U.S. JOLTS job openings

- Japan leading economic indicators

- Japan BoJ summary of opinions

- Wednesday

- Chicago Fed President (Charles Evans) speech

- U.S. consumer credit change

- U.K. home prices

- Canada PMI

- Japan current account

- China balance of trade

- Thursday

- U.S. jobless claims

- U.S. wholesale inventories

- Canada new housing prices

- Japan GDP

- China inflation

- Friday

- U.S. PPI

- Germany balance of trade

- U.K. balance of trade

- U.K. GDP

- U.K. industrial production

- Canada housing starts

- Canada building permits

- Canada unemployment

- Canada hourly wages