U.S. equity futures pointing to a higher opening and USD rates paring some of its losses sustained during Asia trading hours as the latest in the US-China trade war saga continues. The 2-year U.S. Treasury is trading 2.3bps lower to 1.51% and the 10-year U.S. Treasury is 1.5bps lower this morning to 1.518%. Earlier this morning from the G-7 meeting in Biarritz, France (NY +6hrs), President Donald Trump said ‘the prospects for a deal with China are better now than at any time since negotiations began last year’ after claims that China called ‘our trade people and said let’s get back to the table’. While China’s foreign ministry did not confirm the talks, the editor-in-chief of China’s Global Times denied any phone conversations were had in recent days.

Last Wednesday, the Fed released its July meeting minutes which did little to clear up the confusion as to why exactly did the Fed cut interest rates. The meeting participants agreed, generally, that (1) downside risks had diminished since their June meeting and that (2) the rebound in core inflation reaffirmed that the earlier weakness was “transitory”. (3) Participants also noted that low borrowing costs and high equity prices were based on expectations of future Fed rate cuts.

The official justification for the rate cut was as follows: (1) in response to the slowdown in economic activity, in particular, business investment and manufacturing; (2) the risks and uncertainties from trade policy and slowing global growth, while diminished, “remained elevated”; and (3) lingering concerns that core inflation and wage growth were still too low. Powell closing remarks stated that the rate cut was a “mid-cycle adjustment” and not an extended loosening cycle.

On Friday, from the Jackson Hole (Global Central Bank) Summit, Fed Chair Powell warned that the downside risks have intensified in the three weeks since the July FOMC meeting. Powell went on to state that “the shifts in the anticipated path of policy have eased financial conditions and help explain why the outlook for inflation and employment remains largely favorable”. Market expectations are of a 25bps cut in rates at the September meeting and another 25bp cut at the December meeting. The Fed Funds rate (upper band) is currently 2.25%. If market expectations are correct, we could see a 1.75% Fed Funds rate by the end of 2019. Which begs the question, what will the Fed do if we enter an economic recession?

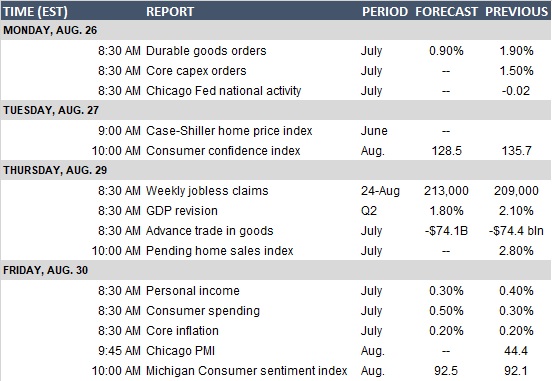

On the data front, durable goods orders came in at +2.1%, beating forecasts of +1.2% and increasing 0.2% MoM. We have consumer confidence on Tuesday, GDP and new mortgage applications on Thursday, and wrapping up the week with PCE inflation data and consumer sentiment on Friday.

See calendar below: