Market Snapshot

The U.S. fixed income market returns today after observing the Columbus Day holiday.

Interest rates and equity futures (DJIA and S&P 500) turning lower after Johnson & Johnson halted clinical trials of its Covid-19 vaccine after a participant fell ill. Meanwhile, the technology-heavy NASDAQ index futures continue to carry the market higher.

It’s Q3 2020 earnings season where according to Factset “estimated earnings will decline for the S&P 500 by -20.5%.” Kicking off earnings season today for banks are JPMorgan and Citigroup. Of particular interest to Analysts will be estimated loan losses due to the impact of COVID-19 and how potential regulatory policy changes, following the election, may affect companies.

Interest Rate Swap Discount Transition

After the close of business on Friday, October 16, clearinghouse operators LCH and CME are both scheduled to begin the transition from Fed Funds to SOFR for USD interest rate swap discounting.

Inflation Trade

After the recent data from the Commodity Futures Trading Commission (CFTC) and the Chicago Board of Trade (CBOT) showed investment managers positioning for a steepening of the yield curve, 10-year rates continued its climb higher. As the risk of contested elections subsides due to recent polls of a “Democratic sweep” in the upcoming elections, inflation fears are pushing long-term rates higher as investment managers expect supersized fiscal spending.

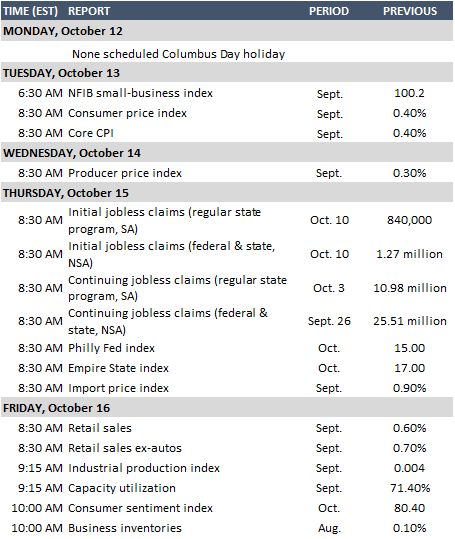

Market participants and policymakers will gain insight on the latest reading of inflation as consumer and producer prices this week.

While some economists forecast the 10-year Treasury yield to end the year above 1%, we caution the rapidly evolving risk and reward from the election landscape as investors pile into the trade.

Will the Fed cap interest rates?

Minutes from the Federal Open Market Committee’s September 15-16 meeting last Wednesday showed the Fed’s willingness to reassess how the Fed could best support its dual-mandate objectives of maximum employment and stable prices (2% inflation).

- The committee agreed to continue its Treasury and MBS purchases at the current pace of $120 billion a month.

- The economic outlook is predicated on additional fiscal support. A scenario where little to no fiscal stimulus in the near-term or a significantly delayed stimulus would slow the economic recovery.

With short-term rates already range-bound between 0% and 0.25%, some officials signaled they would be ready to alter or increase asset purchases – possibly at the long end of the yield curve. The next meeting will be a day after the U.S. elections on November 4-5.

Weighing heavily on the broader market are:

- The U.S. November Elections

- Investors and traders are bracing for a volatile election year as the ultimate Presidential and Senate winners may not be known until December, pushing out typical November hedges into December and January 2021.

- U.S. fiscal stimulus package.

- President Trump’s team proposed a $1.8 trillion stimulus package though House Speaker Nancy Pelosi rejected the counterproposal.

- We may see long-end rates push higher, on inflation expectations, should Congress agree on a $2 trillion+ fiscal stimulus plan.

- U.S.-China relations, as both countries fight on everything from trade to defense issues, monetary policy, and the coronavirus.

- Second Coronavirus wave.

- While there are numerous potential COVID-19 vaccines and therapeutics currently being developed, the limited production capabilities, timing, and acceptance for people to receive the medical solutions are of concern and could be drawn out to the end of 2021.

Up ahead this week: